Directly From My Lenders Mouth!

Mike Meena

Augusta Financial

661-290-2970

We have been touting a first-time buyer tax credit for over a year now that helps buyers qualify for loans and it also gives them a TAX CREDIT in addition to the normal tax write off. The maximum loan amount in Los Angeles, Orange and Ventura Counties is $585,713.00 and it can be used on FHA, Conventional, VA and USDA loans. A first-time buyer is defined as someone who has not owned a property in 3 years. You would be eligible if your household income meets the following criteria:

- LA County $108,120.00 for a 1-2 person household and you can earn up to $126,140.00 if you have a household of 3 or more people.

- Orange County $125,160.00 for a 1-2 person household and you can earn up to $146,020.00 if you have a household of 3 or more people.

- Ventura County $119,880.00 for a 1-2 person household and you can earn up to $139,860.00 if you have a household of 3 or more people.

- call for other county limits

So if you have a first-time buyer and they are saying, "Oh no, my payment is too much," then you throw the following info at them:

$470,000.00 Purchase Price 3.5% down rate 4.375% (5.54APR) No Points

| Principal and Interest | $2301.85 |

| Property Taxes | $490.00 |

| Homeowners Insurance | $90.00 |

| Homeowners Association ??? | $0.00 |

| PMI | $326.56 |

| Total Payment = | $3208.41 |

Here is how this breaks down in a nutshell: $3208.41 - $335.00 = $2873.41. Just this little tax credit makes a 4.375% rate look like a 3.09% interest rate!

YES the money is a straight TAX CREDIT! Not a tax deduction! A TAX CREDIT! This will help a lot of buyers, that could not qualify before, qualify now! The fee is $300.00 and it is the best deal running out there! Please let me know if you have a first-time buyer that is struggling to qualify or crying about higher interest rates!

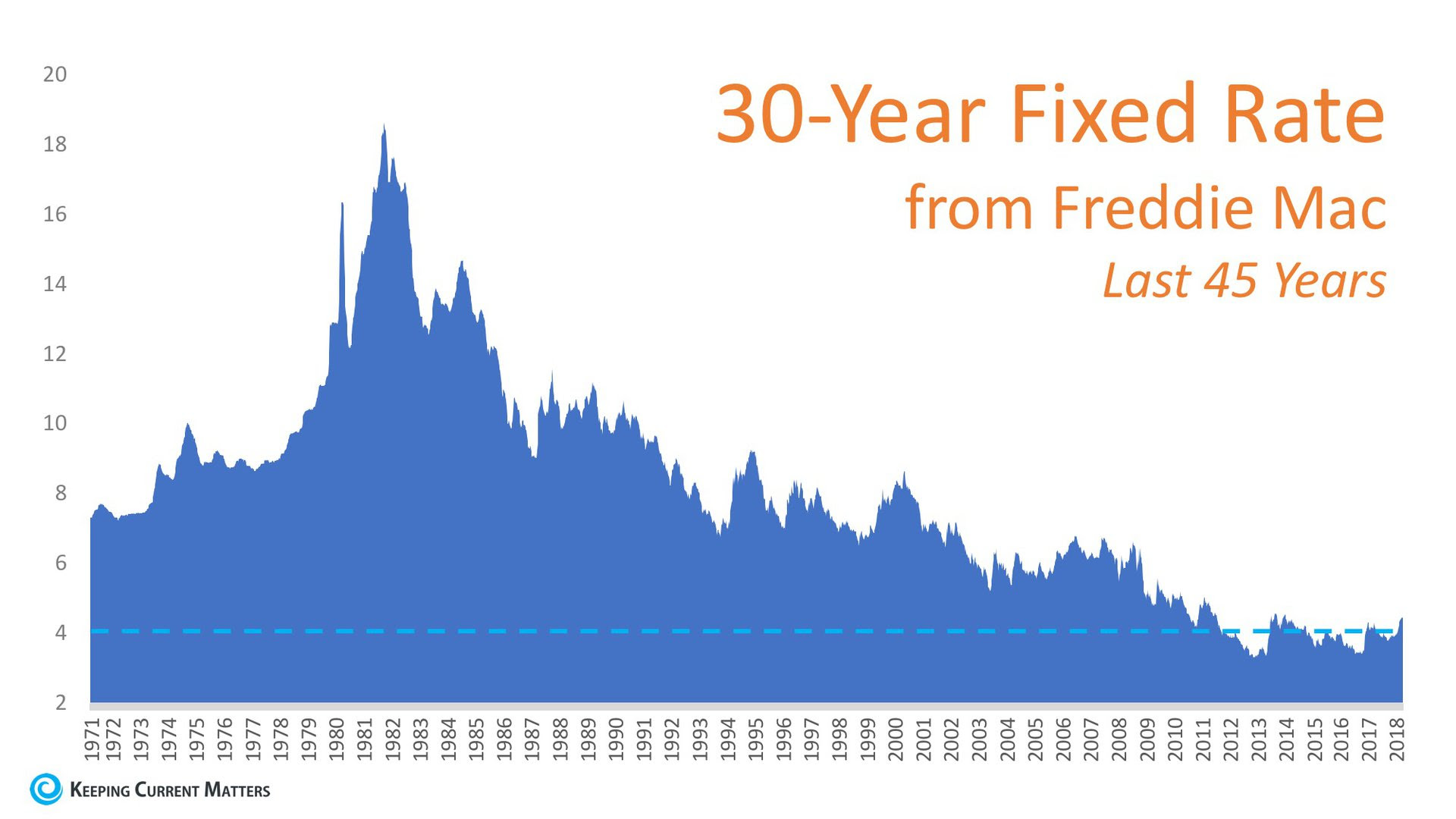

Interest rates rose a little more over the last week. The 30-year mortgage has had 101 months below 5% in the past 60+ years! I hope these help you if you are shopping around:

- 30-year fixed conventional 1st Mortgage with 20% down - 4.750% (4.813 APR). Loan amounts up to $453,100.00 = $2363.58

- 15-year fixed conventional 1st Mortgage with 20% - 4.250% (4.352 APR). Loan amounts up to $453,100.00 = $3408.57

- 5/1 ARM 1st Mortgage - 20% down - Fixed for 5 years and then becomes variable - 4.125% - (4.276 APR) Loan amounts up to $453,100.00 = $2195.95

- 7/1 ARM 1st Mortgage - 20% Fixed for 7 years and then becomes variable - 4.375% - (4.528 APR) Loan amounts up to $453,100.00 = $2262.26

- 10/1 ARM 1st Mortgage - 20% Fixed for 10 years and then becomes variable - 4.375% - (4.528 APR) Loan amounts up to $453,100.00 = $2262.26

- 30-year fixed 1st Mortgage FHA loan 3.50% down - 4.375% (5.539 APR). Loan amounts up to $453,100.00 = $2301.85 + $326.56 PMI = $2628.41

- 30-year fixed 1st Mortgage VA loan 0% - 4.375% (4.318 APR). Loan amounts up to $453,100.00 = $2262.26

- 30-year fixed 1st Mortgage Jumbo loan 20% down - 4.625% (4.639 APR). Loan amounts up to $3,000,000.00 = $15,424.19

All of the above are based on a 740 credit score. Rates are subject to change without notice.

If you have any questions, don't hesitate to contact me directly at 661-510-5370 or call Mike Meena at 661-290-2970.

In many markets across the country, the number of buyers searching for their dream homes greatly outnumbers the number of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

In many markets across the country, the number of buyers searching for their dream homes greatly outnumbers the number of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.